Chapter 20 - Commercial Real Estate

Learning Objectives

At the completion of this chapter, students will be able to do the following:

1) Define capitalization rates and explain how they are used to value income producing properties.

2) Explain the purpose of a pro-forma.

20.1 Introduction to Real Estate Investing

Transcript

As a real estate agent, your goal is to sell homes. However, to do this job well, you will need to learn who your clients are, and even more importantly, why they are buying. Once you understand their needs and motivations in buying real estate, you can make better decisions about which properties to show them. That saves them time and helps the buyer to see value in working with you.

Real estate investing has been a popular vehicle to wealth building for decades. It provides a number of key benefits to buyers and a variety of ways to grow wealth. Agents must be able to sell the house – though understanding why one property is a better fit than another is important. Let's first take a look at the "why's" of real estate investing.

Where does the wealth come from?

For most investors, there are two specific benefits. Real estate investors are looking to benefit from the cash flow they get from the property. This may be in a rental agreement, for example. It may also be in purchasing and flipping a home. Second, they also invest for the long-term appreciation. That is, they benefit as their ownership lengthens because the value of the home, in most cases, grows. This is equity and it is a powerful component of the investment.

You'll learn that this wealth building is not always simplistic and it should never be thought to be such. In fact, many times, your buyers will want to know the potential future value of any real estate investment not just from building equity, but also in the rent they will be able to charge and the investment potential in flipping. Your ability to provide this type of insight will be a key component of the potential success you'll have in the industry when working with these buyers.

Real estate investors are not just large groups. Most real estate agents will find themselves engaging with a wide range of types of buyers. This includes small investors looking to buy just one home. It also includes people who are buying for Real Estate Investment Trusts, or REITs. The investments range from a small purchase of vacant homes to billions of dollars in capital invested in a large investment fund.

That should excite you. You'll work with a wide range of people and have opportunities to see a range of investments made. Not every investment is a solid one. There will be instances in which some transactions will be less than desirable. Yet, it is your job to help your buyers to make decisions that will ultimately benefit them within their financial goals.

Let's talk about the key reasons to invest in real estate. No matter who the buyer is, there are numerous potential reasons to buy.

The first is as a hedge against inflation. Real property – real estate – is an excellent tool for hedging against inflation. Many people realize that, over the long term, real estate grows in value consistently. It grows in value, generally, at a higher rate than inflation as well. Even though the market suffered significant damage in the mid-2000's, it is recovering, for example. That's an important reason many people move into real estate when they worry about other types of investing. It is less volatile than stocks. It is more reliable than other types of investments.

Next, there are numerous tax benefits associated with real estate. Later, we'll talk more about these. But, consider the simple home investor. This is just a person who buys a home to live in. Much of the interest they pay on their mortgage is an income tax deduction. It reduces what they will pay every year in income tax. Multiply this several times for larger investments and additional properties and it is clear there is profit potential here.

And, again, there is the benefit of holding onto real estate. It is a long-term investment that offers low risk. The investment in real estate does not create an instant profit. However, maintained long term, it is a low-risk way of growing wealth.

When you consider each one of these facts, it is clear that there are real benefits to buying property. Whether it is in the purchase of a single home to create rental income or a large investment in commercial real estate, every transaction offers many different opportunities for buyers.

As a real estate agent, it will be a component of your job to help your buyer to find property that will offer a potential financial reward. You will need to educate your buyer on the current value of the property and work to factor in long-term potential.

Key Terms

Capitalization Rate

The rate of interest which is considered a reasonable return on the investment, and used in the process of determining value based upon net income.Capitalization Rate = NOI / Purchase Price

Yield

A return on investment.

20.2 Characteristics of Real Property Investing

Transcript

Real estate agents need to get inside the minds of their clients. To know which properties to present, it becomes essential to understand how investors think about real estate and the investments they want to make. The more effective an agent is at understanding this, the more likely that agent will be able to continue to work with and impress real estate investors in the area.

At the end of the day, the investor is looking for real estate that provides the highest rate of return on their invested capital. This is then balanced with the right level of risk – which ultimately they define. It sounds simple, but navigating hundreds of property listings to find the best match-up for your client is not always that simplistic.

First, consider risk, perhaps the hardest component to the process of selling to investors.

Every investor is going to work hard to manage his or her risk. Risk, in this instance, can be defined as the ability of any property to actually produce an expected cash flow, profit, or value to the investor. That's not to say that investors are always on the lookout for low-risk properties. In fact, many of the most lucrative and successful real estate investors focus instead on properties that offer the greatest level of potential reward. And, that comes with higher risk.

In real estate, often the higher the risk of a property is, the higher the potential for returns. And, when selected properly, the higher the expectations of the buyer.

How do you know how much risk is present, then? There are a variety of factors that can provide insight into this information. For example, cap rates are often a good indication of risk. Cap rates, or capitalization rates, are a ratio of the Net Operating Income, or NOI of a building, divided by the value of the property. For example, if the property is on the market for $2 million, and it generated a net operating income of $200,000, it would have a cap rate of 10%.

The higher the cap rate is, the higher the risk is. The lower the cap rate, the lower the expectation of risk. A lower cap rate on a property will produce a higher valued property. That's because the investor will pay more for the reduced level of risk present – in short, the lower the cap rate on a property, the higher the value of the property.

A multi-family property that is in a less-than-desirable neighborhood is likely to have a higher cap rate. This means it has more risk. The higher cap rate will lead to a lower purchase price.

Next, let's consider the time value of money.

The time value of money, or TVM, is an essential component for evaluating all types of commercial real estate listings when the buyer is an investor. This concept holds the belief that "money in hand" or money that's available on hand is more valuable than money that is given or earned in the future.

A simplistic example is this. If people were given the choice to receive $100 today or $110 in a year from now, most people would rather receive the $100 today. Investors can use this information as a way to measure and project the overall profitability of any type of real estate. This is important to most investors who are considering mid- and long-term investments in property. In short, a buyer needs to consider if the future potential earning of a property is worth more than having money in hand right now. Is it worth the risk?

Cash flow that's earned in the future will be worth less than cash in the present, which means these cash flows are discounted at the minimum rate of return the investor is willing to take. This discount rate helps the investor to measure the net present value of any property.

There's also the concern of liquidity.

Real estate in general is an illiquid asset. There is no easy way to sell property fast to recoup the investment. This is very much unlike stocks which can be quickly sold on the stock market when there is a need for cash on hand. Keep in mind that many investors do not see their real estate as this type of investment and do not expect it to be. However, they should know the market trends and understand expectations now and in the long term about the ease or difficulty of selling.

Consider leverage as another important characteristic of real estate investing.

Leverage is the use of borrowed capital, such as a mortgage, to increase the potential return of any investment. In other words, an investor is using another person's or company's money (OPM) to make an investment. This is a very important aspect of investing. It lets the investor increase their rate of return on any property, but comes at a cost, of course.

For example, if an investor purchases property for $1 million using all cash and the property has a net operating income of $80,000, he has a solid 8% return per year on the money he invested in the property. However, if that same buyer purchases the same property using a $750,000 mortgage, he only pays $250,000 upfront. This reduces the amount of capital the investor has to provide. If that mortgage has an interest rate of six percent, that would mean a monthly mortgage of $4,500 or $54,000 annually. So, that $54,000 needs to be subtracted from the potential net operating income of $80,000. This yields $26,000. In this example, the investor's rate of return is 10.4 percent. Simply divide $26,000 by $250,000. This allows for the investor to grow his or her rate of return from 8% to 10.4%.

Of course, leverage is not always a good thing. In this example, we see positive leverage. It helps to increase the buyer's rate of return on the investment. However, there is also the potential of negative leverage. It decreases the investor's rate of return. How is this determined?

Simply put, when the cap rate of an investment is higher than the interest rate on the mortgage, you can expect that the investor will see positive leverage. Conversely, if the cap rate is less than the interest rate of the mortgage, this creates negative leverage.

What's your job in this? Generally, agents will need to be able to understand each of these components so that they can provide insight into the profit potential of any type of investment. It may mean spending a bit of time working on math, but in the end, it allows you to help your buyer to see better results on any investment they make.

Key Terms

Leverage

The use of borrowed capital (mortgage) to increase the potential return of an investment.

Time Value of Money

The idea that money available at the present time is worth more than the same amount in the future due to its potential earning capacity.

20.3 Key Terminology

Transcript

In this lesson we will cover some of the key terminology that is commonly associated with commercial properties.

Let’s start with net operating income.

Net operating income, also known as NOI, refers to the income a property produces before debt service and any capital expenditures. NOI is expressed on an annual basis. It equals the effective gross income (which is the actual income generated from the property) minus any expenses. For example, if a property has an effective gross income of $1,000,000 and $450,000 in expenses, the NOI would equal $550,000. This is a very important number for a real estate investor because, as we will see in a minute, it is used to determine the value of a commercial property.

Next, let’s cover capitalization rates.

Capitalization rates, also known as CAP rates, refers to the rate of return on a real estate investment based on the net operating income of a property. CAP rates are used to determine the value of a property. The CAP rate is found using the following formula:

CAP Rate = Net Operating Income / Purchase Price (or current market value)

For example, if a property is being purchased for $2,000,000 and has an NOI of $150,000, the CAP rate would equal $150,000 divided by $2,000,000, or 7.5%.

You can also use this formula to determine how much one should pay for a property.

For example, an investor is looking to purchase a property with an NOI of $100,000. They want to purchase the property at no more than a 6% CAP rate. The most they would be willing to pay is $100,000 divided by 0.06 or $1,666,667.

The next key term we’ll cover is return on investment, also known as cash on cash return. This represents the annualized return an investor will earn on their initial cash investment. For example, if an investor puts up $400,000 to purchase a property that generates $40,000 in profit the first year, the investor would get a 10% cash on cash return in year one. Going back to capitalization rates, if the investor were to purchase a property using all cash, the cash on cash return would equal the capitalization rate for year one.

An investor’s return on investment is a key metric, as it can be used to compare investment opportunities. For example, if an investor has the opportunity to purchase stocks in a company with a projected return on investment of 6%, versus a commercial property with a return on investment of 8%, the investor can more clearly see that the real estate opportunity is a better option.

Next, we’ll discuss the difference between equity and cash flow. The net operating income is the cash flow from a property; however, there is also value in the property beyond cash flow, which is equity. Equity equals the current market value of a property minus the loan balance. For example, if a property is valued at $1,000,000, but there is an existing mortgage of $700,000, the equity will equal $300,000 ($1,000,000 minus $700,000).

Initially, the equity in a property equals the investor’s down payment. But, as the cash flow in the property increases over time, so does the value of the property. This means the investor’s equity will grow beyond their initial down payment. While equity is value on paper, it can only be realized if the investor sells the property or opts to refinance the mortgage.

Finally, we’ll discuss pro-formas. A pro-forma is an income and expense statement for a property. It is produced by an investor and typically shows the current income and expenses for a property along with future projections, based on the investor’s knowledge of the real estate market. Overall, the pro-forma gives the investor a more in-depth look at a property. The investor uses this document to determine the financial performance of a property and if the property would make a viable investment. The key terms we discussed in the lesson are included in a pro-forma, along with several other details.

That being said, let’s go to the next lesson, where we will review a pro-forma in detail.

Key Terms

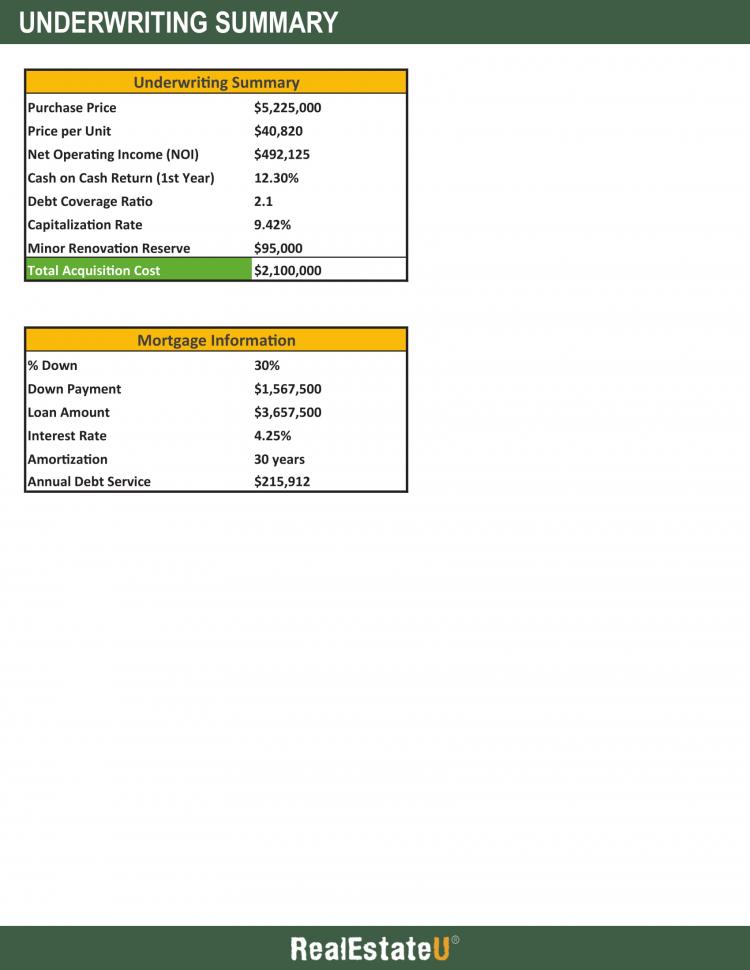

20.4a Underwriting Summary

Please spend a few minutes reviewing the document below.

20.4b Pro-Forma

Please spend a few minutes reviewing the document below.

20.4c Exit Strategy

Please spend a few minutes reviewing the document below.

20.5 Pro-Forma Analysis

Transcript

In this lesson, we will review a multi-family acquisition from the viewpoint of an investor. This will give you a better idea of how investors analyze investment properties and what they look for in determining if a property is worth buying or not. Real estate investors are looking for a return on their investment. This is very different from single-family home buyers, who buy based on emotions, proximity to schools, quality of the neighborhood, etc.

Let’s start by reviewing the property.

The property is a 128-unit multi-family complex, that consists of eight separate buildings surrounding an interior courtyard. The rental units consist entirely of 1- and 2-bedroom apartments. The property is stable with a 97% occupancy rate.

The property is considered a class-B multi-family asset in a class-A neighborhood. Let’s take a minute to review what these classes mean. Properties can be classified in three different classes, Class A, Class B, and Class C. Class A assets are typically the newest and best buildings in a neighborhood. They are typically less than 10 years old and include a full range of amenities. Class B assets are anywhere from 11 to 25 years old with some amenities. Overall, the property is still in good condition, but just not as nice as a Class A asset. Class C assets are 25 years plus in age. They typically have little to no amenities. Overall, these assets are outdated and in poor condition.

In terms of neighborhoods, Class A neighborhoods are considered the best. These neighborhoods are well maintained, offer good transportation, good schools, have low crime rates, and typically have the most expensive properties. Class B neighborhoods are still considered good neighborhoods, but the infrastructure, schools, and overall quality of properties is not as good as a Class A neighborhood. Class C neighborhoods are considered the least desirable neighborhoods.

In our example, the investor wants to purchase a property in the best neighborhood; however, they don’t necessarily want the best property in the best neighborhood. The reason being is that a Class B asset has room to increase in value while the desirability of the surrounding neighborhood will allow the investor to increase rents overtime.

The investor’s strategy is to upgrade the property, increase the rents and add additional sources of income. The investor is also looking to decrease expenses by hiring a new management company to run the property more efficiently.

Now that we know a bit more about the property and the investor’s game plan, let’s go into the basic setup of the deal.

The investor is looking to purchase the property for $5,225,000, which amounts to $40,820 per unit. The current net operating income is $492,125, which gives us a capitalization rate of 9.42%. This is a very high cap rate for a Class B property in a Class A neighborhood. Besides the down payment and closing costs, a minor renovation reserve of $95,000 will need to be set aside for a few cosmetic upgrades to the apartments. In total, the investor will need to make a cash investment of $2,100,000 to purchase the property.

Next, let’s go over the mortgage information for the property. The lender requires a 30 percent down payment, which amounts to $1,567,500. The loan is 30-year fully amortizing, in the amount of $3,657,500 with an interest rate of 4.25%. This gives us an annual debt service of $215,912. Overall, these are very favorable financing terms for the investor. A jumbo loan of this amount typically commands a higher interest rate from the lender. If needed, such favorable financing terms gives the investor the ability to pay a slightly higher purchase price and still reach their return on investment goals for the property.

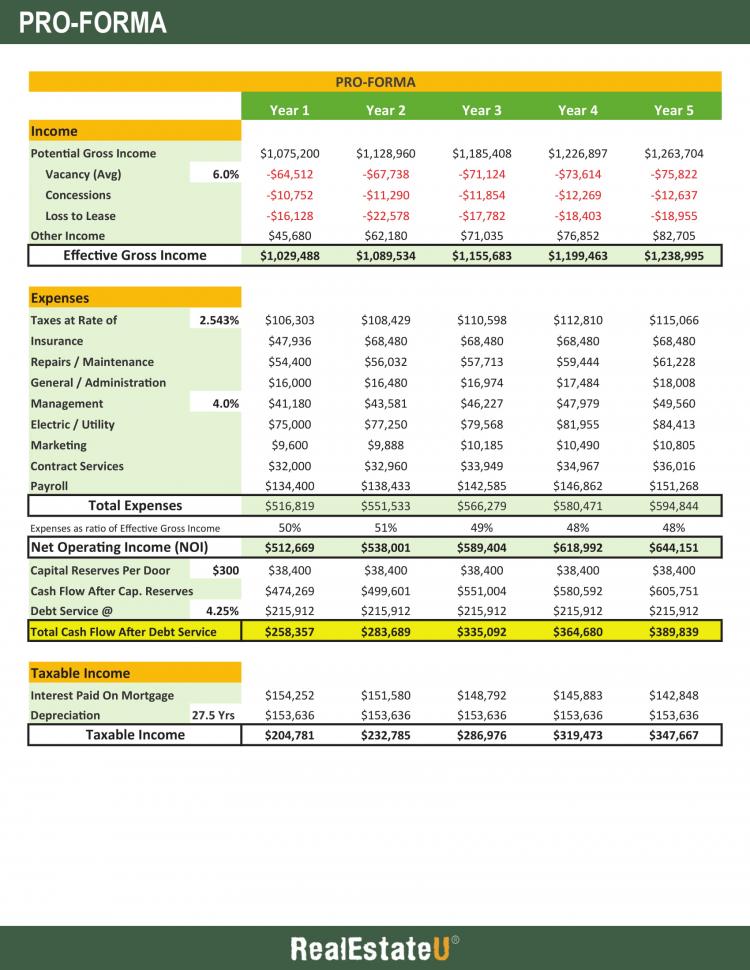

Now that we know some of the basic acquisition and financing numbers for the deal, let’s dive into the investor’s pro-forma for the property. This is a document that the investor produces, which shows how they think the property will perform in the near future. It’s important to note that while some of the numbers are more straightforward, such as the annual debt service or the amount paid in taxes, most of the numbers are based on assumptions by the investor. Based on their experience, they have to try and predict where they think the income and expenses will be in the future. Ultimately, the accuracy of this document is only as good as the investor’s assumptions.

That being said, let’s go through the pro-forma and explain how the investor is generating their income and expense numbers for the property.

First, we’ll go over the property’s income. The top line of the income is always the potential gross income. This number represents what the property will earn if all of the units were 100% occupied. It’s the most the property can generate in income from rent. We will see this number steadily increase over the next 5 years. This is due to an anticipated rent increase each year. The investor plans to raise rents by 5% for the first two years, followed by a 3.5% and 3% rent increase in the last two years. The investor assumes this because of the quality of the neighborhood. The rents are currently under valued and the demand for the neighborhood is high enough to steadily increase rents.

While the potential gross income assumes a 100% occupancy rate, this is unrealistic. Even in the best buildings, a management company needs a month or two to complete minor repairs and renovations and find a new tenant after the old tenant moves out. You must take into account vacancy, concessions, and loss to lease.

In our example, the investor is assuming a 6% vacancy factor. This represents the potential income that is not realized because a unit currently does not have a tenant. A 6% vacancy factor is conservative for this building, especially since the existing vacancy rate is only 3%, as mentioned earlier in the lesson.

Next, we have concessions. Concessions represent discounts that the management company may offer to prospective tenants to entice them to rent an apartment as quickly as possible. A common example of a concession is offering the tenant the first month’s rent for free. In this case, the investor is assuming they will offer a total of 1% of the potential gross income in concessions each year.

After concessions, we have loss to lease. This number represents the amount of rent below what the landlord could collect if the apartments were rented at full market value. For example, if an apartment is currently being rented for $900 per month but has the potential to be rented for $1,000 per month, the loss to lease would equal $100 per month. Sometimes even a concession is not enough to entice renters, so the landlord will have to drop the rent. This occurs even in the best buildings. Perhaps a tenant moves out during the winter months when the rental market is slower, and the landlord does not want to wait until the spring time to find a new tenant. They may then be forced to drop the rent below market value to attract a new tenant more quickly. In our case, the investor is assuming a loss to lease of 1.5% of the potential gross income.

The last line item from the income section is ‘other income’. This represents additional revenue the investor can collect beyond rent. A common example includes laundry facilities for the tenants. In our case, the investor plans on adding storage units and additional parking spaces that will be rented out to the tenants. The investor assumes the additional income will amount to 4.2 to 6.5% of the potential gross income.

Finally, we get to the effective gross income. The effective gross income equals the potential gross income, minus vacancies, concessions and loss to lease, plus other income. Always remember that potential gross income is the top line item for income, while effective gross income is the bottom line. Effective gross income represents the actual income collected from the property.

Next, let’s cover the expenses section of the pro-forma.

First up are property taxes. The tax rate is set at 2.543%. This is a total combined tax rate that includes city, county and school district taxes. It’s important to remember that the tax rate is applied to the assessed value, not the market value. In our case, the assessed value at year 1 is $4,180,220. The investor then assumes the assessed value, and thus the amount paid in property taxes, will increase at 2% per year.

Next, we have property insurance. The amount paid in insurance will jump in year 2 as the value of the property increases. The investor can shop around for the best insurance rates and lock in a multi-year deal.

Repairs and maintenance refer to smaller items that need to get fixed on a day-to-day basis. For example, changing light bulbs, touching up paint in the hallways, or preventative maintenance items such as changing an air conditioning filter. The investor set the repairs and maintenance budget at $54,400 and assumed a 3% increase each year.

Administrative fees are assumed to be $16,000 in year one and then increase at 3% per year.

Next, we have the property management fee, which is set at 4% of the effective gross income. Property managers typically charge a fee as a percentage of the property’s income. As the income increases, so does the management fee. Most owners will hire a property manager to run the day-to-day operations of the property. The property manager is responsible for maintaining the property, finding new tenants, dealing with tenant related issues, and trying to increase the overall value of the property. This allows the investor to be hands-off from the property after closing, which frees up their time to find other investment properties. It’s always important for investors to work with competent property managers, otherwise the wrong property manager can actually decrease the value of the property.

Next, we have electric and utility expenses. These typically include electric, gas and water bills for the common areas of the property. The tenants will be responsible for paying their own electric and gas bills. Like the administrative and maintenance expenses, electric and utility expenses are assumed to increase at 3% per year from the base amount of $75,000 in year one.

Next, we have marketing expenses. These are expenses incurred trying to acquire new tenants. In this case, the marketing expenses will mostly include online advertising since the management company has their own in-house broker in charge of leasing. Some management companies will hire real estate brokers to find new tenants. In that case, the marketing fee will primarily consist of the broker’s commission since the broker will be responsible for paying any advertising expenses. The investor is also assuming the marketing expenses will increase at 3% per year.

After the marketing expenses, we have contract services. This includes companies hired to perform various tasks throughout the property. For example, the management company may hire a landscape company to cut the grass and shrubs once a month. The initial contract services budget is set at $32,000 and will increase at 3% per year.

Finally, we have payroll expenses. This includes the salaries for both the full-time and part-time employees who work at the property. It’s important to note that employee salaries are not included in the property management fee. The investor assumes payroll expenses will increase at 3% per year, which represent employee raises.

This gives us the total expenses for the property, which amount to roughly 50% of the effective gross income. This is a typical expense ratio for a multi-family property of this size. If the expense ratio were at 60% it would indicate that the property manager is not running the property effectively.

Below the expense ratio we get the net operating income. This is a very important line item for the investor, because the value of the property is directly linked to this number. Remember, the value of an income producing property equals the net operating income divided by the capitalization rate. One of the investor’s main objective is to increase the net operating income each year. This can be accomplished by increasing income, decreasing expenses, or a combination of both.

That being said, the net operating income is not the actual profit the investor will realize. We must first subtract capital reserves and the annual debt service.

Capital reserves represent major repairs done to the property; however, rather than be stuck with a massive emergency repair bill, for example, replacing a roof for $50,000, the investor will set aside a capital reserve fund for any major expense items. It’s important to note that capital reserve expenses generally increase the value of the property.

In our example, the investor will set aside $300 per unit per year as a capital reserve fund. This amounts to $38,400 per year.

Finally, we must subtract the annual debt service from the net operating income. This represents the mortgage payments made on the loan. Since this is a 30-year, fully amortizing loan, the annual debt service will remain constant at $215,912 per year.

When we subtract the capital reserves and annual debt service from the net operating income, we get the total cash flow after debt service, or net cash flow. This represents the profit from the property.

However, this number is different from the taxable income for the property. We have to take into account the dedications allowed by the IRS. In this case, the investor can write off the interest paid on the mortgage and depreciation.

The interest paid on the mortgage can be provided by an amortization table. Note that the interest decreases each year. This is because the loan balance is gradually being paid down each month.

Even though lenders consider multi-family properties as commercial, the IRS still classifies them as residential, and therefore can be depreciated over 27.5 years. However, the 27.5 years is applied to the building only, which means we need to subtract the value of the land from the purchase price. In our example, the land is assumed to be worth $1,000,000. This gives us $5,225,000 minus $1,000,000 or $4,225,000 as the value of the building itself. Next, we divide this number by 27.5 to get $153,636. This is the amount that can be written off as depreciation each year.

To determine the taxable income, you must subtract the interest and depreciation deductions from the net operating income. We subtract from the net operating income and not the cash flow after debt service because capital reserves are not a tax deductible item, and the debt service includes a principal payment, which is also not tax deductible.

When we do the math, we see that the taxable income is less than the cash flow after debt service, or profit. This highlights one of the major benefits of owning an investment property. Most investment properties serve as a tax shelter for the investor. In some cases, the taxable income on a property can show a loss, which means the investor does not have to pay any income taxes on their profits.

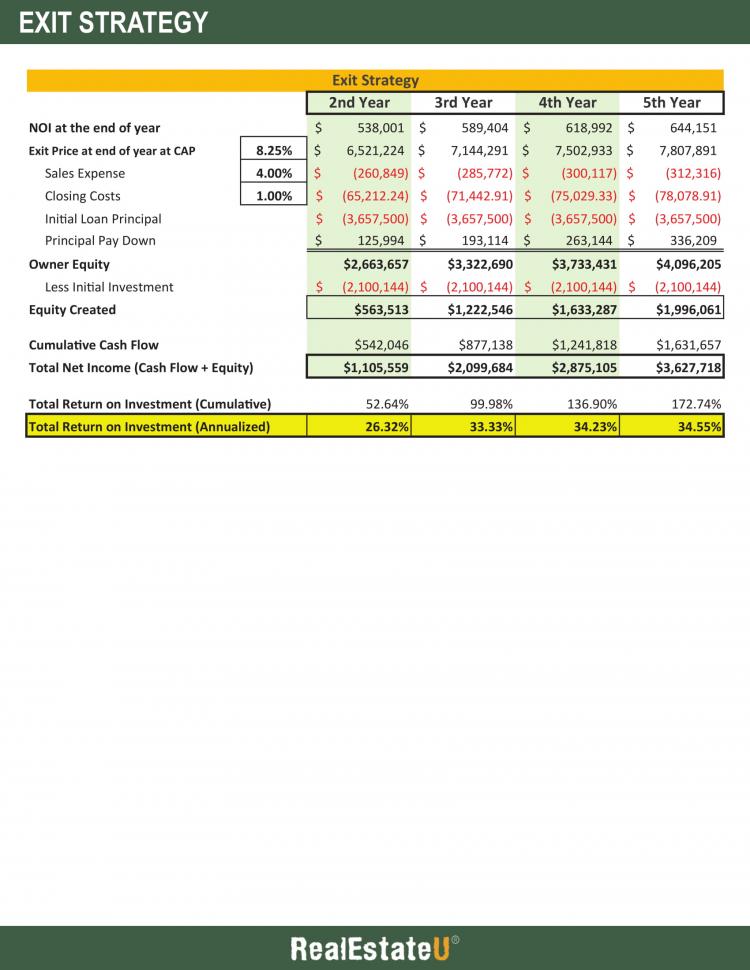

This brings us to the exit strategy, which is the final analysis in our case study. The investor will have to determine at which point they will sell the property. This ultimately depends on their investing goals. They may want to sell the property after a few years and take their equity out to buy a larger investment property. Or, they may want to hold the property and continue to benefit from the yearly cash flow. The investor also has the option of increasing the value of the property to a point where they can refinance the property to extract some of their equity, and then use that cash to purchase another investment property for their portfolio.

Let’s take a look at the exit strategy numbers line by line.

The exit strategy spreadsheet shows the return on investment the investor was to realize if they sold the property after years two through five. It takes into account the net cash flow, the equity gained and the principal pay down to determine the annualized returns.

First, we have to determine the exit price, or the potential sales price at the end of each year. The investor assumes they will sell the property at an 8.25% capitalization rate. To find the sales price, we simply divide the net operating income from the first line by the capitalization rate.

Next, we have to subtract the expenses related to the sale of the property. These include the sales expenses and closing costs. The sales expense primarily consists of the broker’s fee and attorney fees, while the closing costs consist of more general expense items. The investor assumes the total closing expenses will amount to 5% of the sales price.

Next, we have to subtract the initial loan amount, but we add back the principal pay down that has accumulated. You have to remember that the mortgage payments slowly pay down the loan balance, which essentially become equity for the investor. While most of the mortgage payments in the first several years of the loan consist of interest, there is still some equity gained. This is listed as $125,994 after year two and $336,209 after year five. This information can be obtained from an amortization table.

When we subtract the sales expense, closing costs, and initial loan principal, and add back the principal pay down, we get the owner’s equity. However, we then have to subtract their initial investment in the deal to get the net equity or equity created. This represents a net increase in the value of the property, which can only be obtained when the investor sells the property or opts to refinance their mortgage.

We also have to take into account the cash flow the investor collected over the years. The cumulative cash flow lists the amount of cash received from the current year plus the previous years. For example, the cumulative cash flow at the end of year three includes the cash flow from year three, plus the cash flow from year two and year one.

When you combine the equity created and the cumulative cash flow, you get the total net income. Next, when you divide the total net income into the initial cash investment of $2,100,144, you get the cumulative return on investment. However, most investors want to know how much they will earn on an annual basis, rather than a cumulative basis. To find the annualized return on investment, we must divide the cumulative return on investment by the number of years the investor owned the property. For example, if the investor elects to sell the property at the end of year four, the cumulative return on investment will be 136.90%. We must then divide this number by four years to get an annualized return on investment of 34.23%. This means the investor will earn a 34.23% return on their initial $2,100,144 cash investment for each of the four years. Also, remember that the taxable income is less than the actual income, which means the investor will be paying less in taxes on their profits from the property. In other words, the after-tax cash flow for the investor will be greater compared to other investments because of the tax shelter nature of commercial real estate.

When you look at the return on investment over five years, you can start to see potential options for the investor. Since the return on investment is steadily increasing each year, the investor may elect to hold on to the property and benefit from the yearly cash flow. The investor will have to evaluate the market conditions and determine if the rental market will continue to grow over the next several years.

Another option may be to refinance the property after five years. At the five year mark, the investor will have created nearly $2,000,000 in equity, which can be taken out of the property by refinancing the mortgage. This gives the investor the option to continue benefiting from the yearly cash flow while also getting cash to purchase another investment property.

Finally, the investor can sell the property entirely and use the profits to purchase an even larger property using a 1031 exchange. A 1031 exchange will allow the investor to avoid paying capital gains as well as having to pay back the deprecation that was deducted. In other words, a 1031 exchange gives the investor a tax shelter just by purchasing another investment property.

So, there you have it, a full case study analysis of an investment property from the eyes of an investor. This will help you better understand how investors value commercial properties. Investors are ultimately buying cash flow and looking to maximum their return on investment. A nice, new looking commercial building may not work for an investor because the numbers behind the building offer too little returns for their financial goals. However, buying into a slightly older, and riskier building may get the investor their desired return on investment.

Ultimately, you have to understand that the mindset behind purchasing a commercial property is very different from that of a residential home buyer.

Key Terms

COPYRIGHTED CONTENT:

This content is owned by Real Estate U Online LLC. Commercial reproduction, distribution or transmission of any part or parts of this content or any information contained therein by any means whatsoever without the prior written permission of the Real Estate U Online LLC is not permitted.

RealEstateU® is a registered trademark owned exclusively by Real Estate U Online LLC in the United States and other jurisdictions.